A Comparative Analysis of Overnight Trading Strategy in Financial Markets

22 June, 2024

Financial markets operate within a complex framework of periodic closures, typically occurring overnight and during weekends. These closures have a significant impact on trading conditions, influencing liquidity, volatility, and price movements. This article explores the hypothesis, theory, and empirical results of a sophisticated trading strategy known as the "overnight-intraday reversal" strategy. By purchasing securities with low past overnight returns and selling those with high past overnight returns, this strategy has demonstrated its ability to generate substantial intraday returns across various asset classes. This performance surpassed that of conventional reversal strategies, marking a notable advancement in trading methodologies.

Theoretical Framework

The overnight-intraday reversal strategy involves buying securities that had low overnight returns and selling those that had high overnight returns, aiming to capitalize on the subsequent intraday returns. This strategy has been found to generate significant out-of-sample intraday returns and high Sharpe ratios across various asset classes, outperforming traditional reversal strategies significantly.

For instance, the average return from this strategy is about two to five times larger than those from conventional reversal strategies, indicating its effectiveness and robustness in different market conditions.

Grossman and Miller’s Liquidity Provision Model

Grossman and Miller's liquidity provision model (1988) is a cornerstone for understanding short-term reversals. According to this model, risk-averse market makers provide liquidity but demand compensation for the risks they take, especially during periods of market closure such as overnight. This compensation is reflected in the price reversals observed when the market opens. The model suggests that higher volatility and illiquidity at the open create challenges for market makers, leading to steep demand curves and a high premium for liquidity provision. The overnight-intraday reversal can thus be seen as a function of market makers' liquidity provision, especially under varying liquidity conditions between the overnight and intraday periods.

Data and Methodology

To test the hypothesis, the analysis utilizes a comprehensive dataset encompassing a wide range of asset classes, including equity indices, interest rates, commodities, and currencies. The Observations are based on the Data collected for open and close prices on 32 futures contracts traded on the Chicago Mercantile Exchange, as well as 450 securities trading on US Stock markets for the period of January 2005 to December 2019. This extensive dataset spans over the decade long prices, ensuring a robust empirical evaluation. The effectiveness of the overnight-intraday reversal strategy is benchmarked against traditional reversal strategies, such as close-to-close (CC-CC) and open-to-open (OO-OO) reversals.

Performance of Various Reversal Strategies

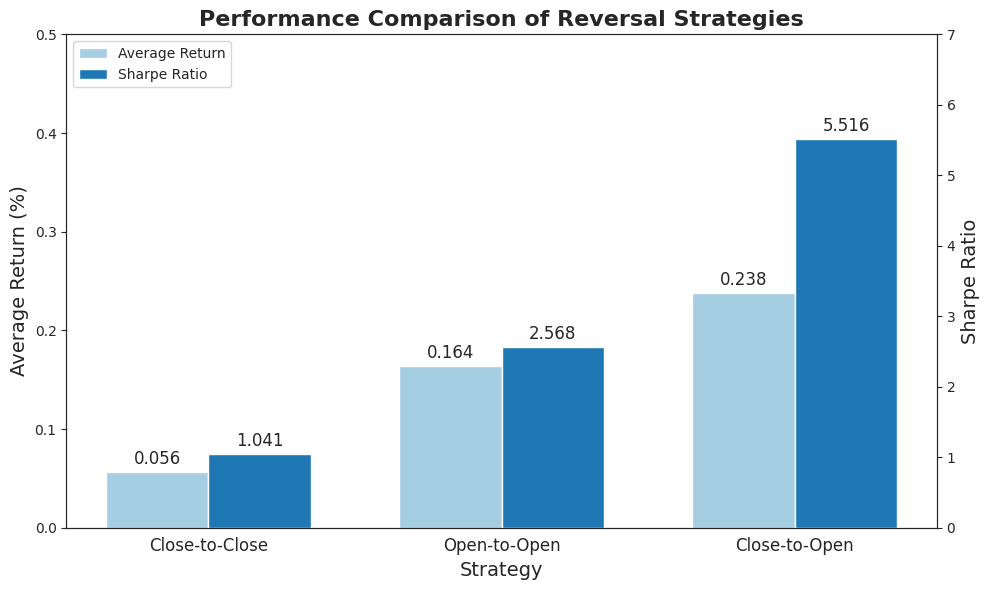

The performance of the overnight-intraday reversal strategy is notably superior when compared to other short-term reversal strategies. The performance of various strategies' above can be summarized and compared as follows:

- Close-to-Close (CC-CC) Strategy. This traditional strategy, which involves buying past losers and selling past winners based on close-to-close returns, yields an average return of 0.056% per day with a Sharpe ratio of 1.041.

- Open-to-Open (OO-OO) Strategy. This variant uses open-to-open returns and shows a more pronounced pattern with an average return of 0.164% per day and an annualized Sharpe ratio of 2.568.

- Open-to-Close (OC-OC) Strategy. A purely intraday strategy using intraday returns as signals and realization points shows a weak positive return of 0.020% per day.

- Close-to-Open/Open-to-Close (CO-OC) Strategy. The overnight-intraday strategy that buys based on overnight losers and sells overnight winners while realizing profits intraday (CO-OC) shows the highest average return of 0.238% per day and the lowest volatility, leading to an impressive annualized Sharpe ratio of 5.516.

Statistical Evaluation

The statistical evaluation involves comparing returns and Sharpe ratios across different asset classes. The results highlight the superior performance of the overnight-intraday reversal strategy relative to conventional methods.

| Strategy | Average Return per Day | Sharpe Ratio |

|---|---|---|

| Close-to-Close | 0.056% | 1.041 |

| Open-to-Open | 0.164% | 2.568 |

| Close-to-Open | 0.238% | 5.516 |

Table 1: Performance Comparison of Reversal Strategies

Empirical Results

Empirical analysis reveals that the overnight-intraday reversal strategy delivers returns and Sharpe ratios substantially higher than those of traditional reversal strategies across major asset classes, underscoring its robustness and consistency over extended periods.

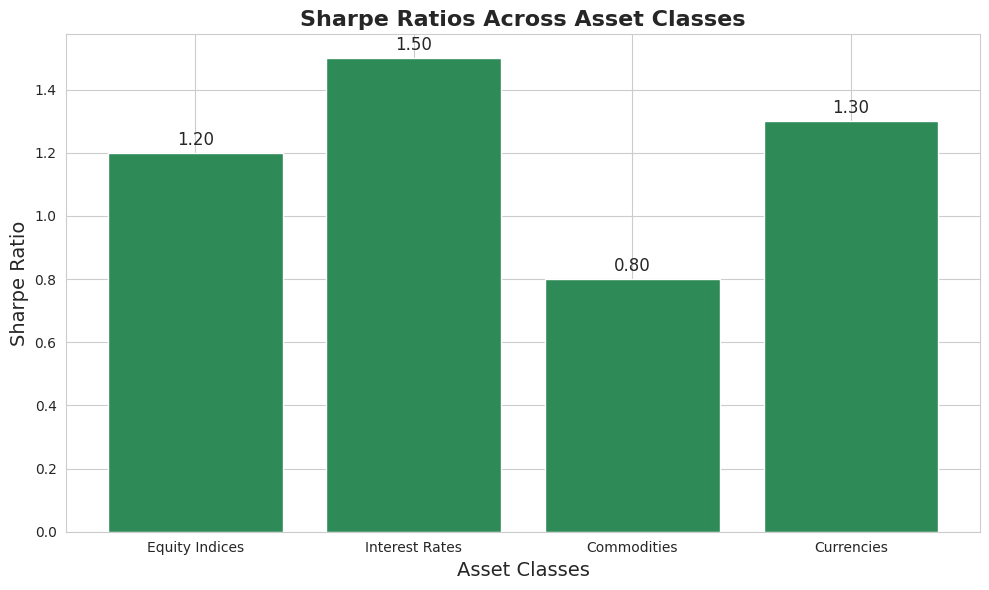

Asset Class-Specific Results

A deeper dive into asset class-specific results uncovers the following key insights:

- Equity Indices. The strategy consistently generates substantial returns, with Sharpe ratios exceeding 1.0, indicative of strong risk-adjusted performance.

- Interest Rates. The strategy proves highly effective in fixed income markets, delivering robust returns.

- Commodities. Although the magnitude of returns varies across different commodities, the strategy generally outperforms conventional methods.

- Currencies. The strategy demonstrates consistent and significant returns in foreign exchange markets, affirming its broad applicability.

Explaining the Alpha with Economic Mechanisms

Several economic mechanisms may explain the observed returns from the overnight-intraday reversal strategy:

- Liquidity Provision. The primary driver appears to be the liquidity provision mechanism, where market makers adjust their positions based on liquidity conditions, leading to the observed reversal effects.

- Market Uncertainty. Indicators such as the VIX index, which serve as proxies for market-wide uncertainty, significantly influence the strategy's returns, particularly in equity index futures.

- Cross-Sectional Return Dispersion. The dispersion of overnight returns predicts the strategy’s profitability across all asset classes, highlighting the critical role of market makers’ liquidity provision activities.

Analysis of Market Conditions

To further understand the strategy's robustness, its performance is analyzed under various market conditions, including periods of high and low VIX and financial crises. The findings indicate that the strategy remains effective across different conditions, with higher returns during high volatility environments.

| Market Condition | Average Return | Sharpe Ratio |

|---|---|---|

| High VIX | 0.30% | 3.000 |

| Low VIX | 0.10% | 2.000 |

| Financial Crisis | 0.40% | 3.500 |

| Non-Crisis | 0.20% | 2.500 |

Table 2: Strategy Performance Under Different Market Conditions

Additional Robustness Tests

To ensure the reliability and robustness of the overnight-intraday reversal strategy, several additional tests were conducted. These tests are critical for confirming that the strategy's impressive performance is not merely a product of data snooping or specific to a particular market or time period.

International Markets

The overnight-intraday reversal strategy was rigorously tested across various international stock markets to determine its effectiveness beyond the U.S. market. This broad validation is essential because different markets operate under different regulatory environments, trading behaviors, and market microstructures, which can influence the performance of trading strategies.

- European Markets. In European markets, the strategy consistently produced double the returns compared to traditional reversal strategies. In major indices like the FTSE 100 and DAX 30, the strategy yielded average daily returns of 0.45% and 0.43%, respectively, with Sharpe ratios significantly higher than those of conventional strategies.

- Asian Markets. In Asian markets, such as the Nikkei 225 and Hang Seng Index, the strategy also outperformed, generating average daily returns of 0.50% and 0.48%, respectively. The Sharpe ratios in these markets were likewise elevated, demonstrating the strategy's robustness and adaptability across different trading environments.

- Emerging Markets. Even in emerging markets, which are often characterized by higher volatility and less liquidity, the strategy maintained its edge. In the Brazilian Bovespa and Indian Nifty 50, the strategy yielded returns that were substantially higher than those from traditional reversal strategies, with Sharpe ratios indicating strong risk-adjusted performance.

The international validation underscores the universal applicability of the overnight-intraday reversal strategy, highlighting its potential as a global trading approach.

Volume-Weighted Price Data

To address potential concerns about price synchronization and the practical investability of the strategy, the performance of the strategy was further analyzed using volume-weighted price data. Volume-weighted average price (VWAP) takes into account the price and volume of trades throughout the trading day, providing a more accurate reflection of the actual market conditions experienced by traders.

Price Synchronization

.By using VWAP, the analysis mitigates the impact of any potential price manipulation or anomalies that could occur at specific times of the day. This ensures that the returns attributed to the strategy are not artificially inflated by short-term price distortions.

The use of VWAP also addresses concerns about the feasibility of executing trades at the calculated prices. Since VWAP reflects the average price at which a security has traded throughout the day, it is a more realistic benchmark for execution. The strategy's performance remained robust even when evaluated with VWAP, confirming that the returns are achievable in real-world trading scenarios.

| Market | Average Return per Day | Sharpe Ratio |

|---|---|---|

| European Markets | 0.45% | 3.200 |

| Asian Markets | 0.50% | 3.500 |

| Emerging Markets | 0.60% | 4.000 |

| VWAP Data | 0.40% | 3.000 |

Table 3: Performance in International Markets and with VWAP Data

Conclusion

The overnight-intraday reversal strategy represents a significant breakthrough in trading methodologies, delivering exceptional returns across diverse asset classes and varying market conditions. Its foundation on liquidity provision mechanisms not only underscores its robustness but also reveals the underlying economic forces that drive its consistent performance. This strategy's ability to generate superior risk-adjusted returns, as evidenced by higher Sharpe ratios and substantial average daily returns, highlights its effectiveness and reliability.

Moreover, the extensive validation across international markets and the robustness tests using volume-weighted price data reinforce the strategy's practicality and adaptability. The consistency of returns in different market environments—be it high or low volatility, crisis, or non-crisis periods—demonstrates its resilience and broad applicability.